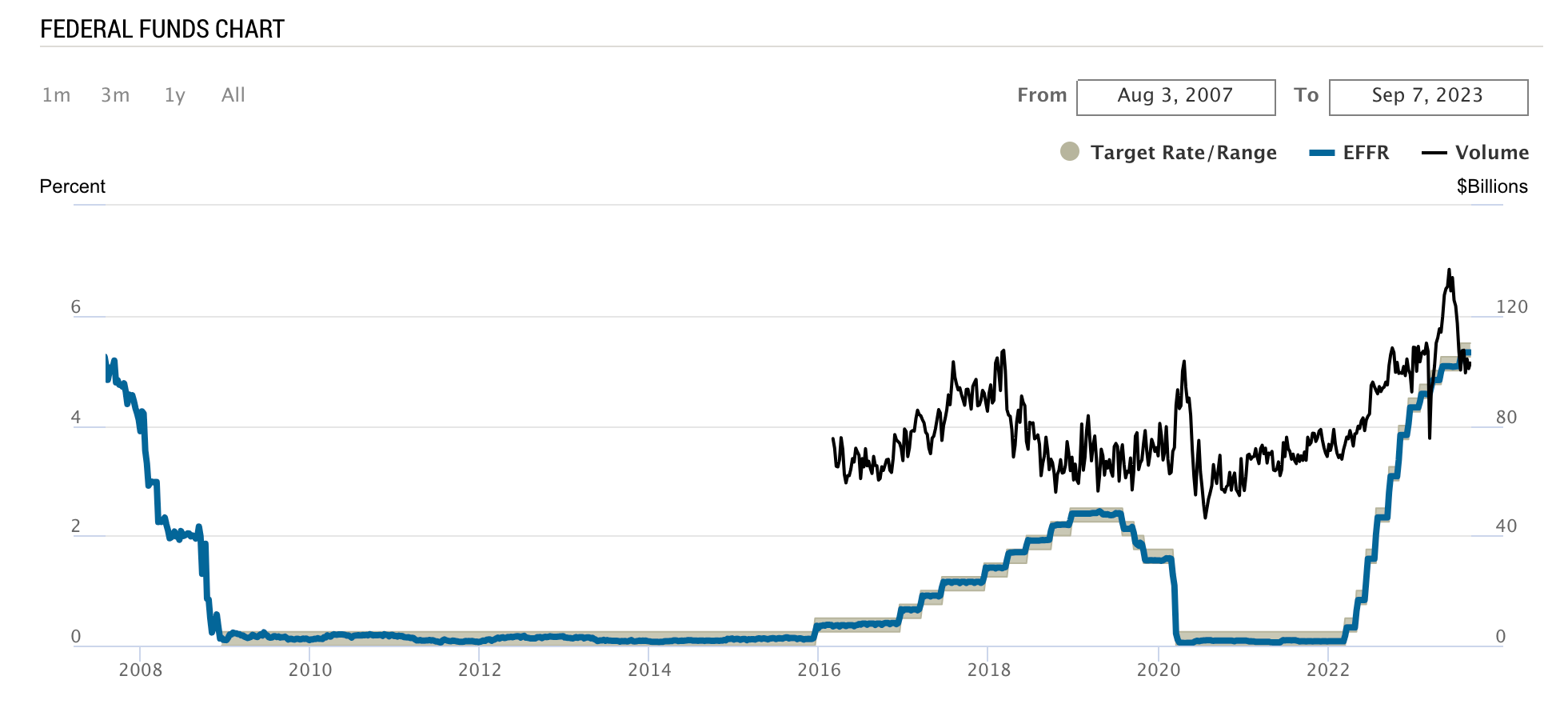

The zero interest rate era started from GFC and extended well into Q1 2022. In a market environment that features zero interest rates and easy access to capital, treasury management takes a back seat as there is no yield really and capital is extremely accessible.

However, things started to change very rapidly as we go deeper into the rate hike cycle. On March 10 2023, twelve months after Fed’s first rate hike, Silicon Valley Bank collapsed after failing to cope with a bank run. To reach for higher yield from the deposits flooding in, SVB had increased its holdings of long-term securities substantially since 2021, accounting for them on a hold-to-maturity basis (in other words, NOT mark-to-market). The swift rate hikes significantly decreased the market value of these long-term securities (recorded as unrealized loss). As the borrowing costs going up, more and more SMEs turned to their cash deposit. To meet the withdrawal requirement, Silicon Valley Bank was forced to sell long-term securities that were deeply in red. When the news came out, it alarmed the investors and aggravated the situation and led to more withdrawals, effectively a bank run. In the digital era where money travels as quickly as information, the bank went under in a matter of days.

Nothing alerts people more than a tragedy that can possibly happen to themselves. The SVB fall, together with other three bank failures happened shortly after, served as a wake up call for all SMEs who hold cash deposits at banks. As the macro environment continues to change, treasury management is back in the spotlight.

In essence, treasury management has two main tasks: liquidity management and yield optimization. Liquidity management is about making sure you have sufficient cash in hand to support day-to-day business operation. Yield optimization is about investing the idle cash to earn highest yields possible without taking excessive risk.

Liquidity management

To manage liquidity effectively, there are three key measures to consider: understand your working capital cycle, arrange short-term borrow facilities if possible, and have some cash buffer.

Understand your working capital cycle. The two magic words for any business to have healthy working capital cycle are “payment terms“. Often times, SMEs get caught up in the headline booking numbers and overlook the payment terms. The reality is, payment term can make or break a SME. Yes, it is that serious. If your account receivable cycle is 60 days and your payable is 30 days, it means that you have to pay your expenses BEFORE you receive revenue from your customers. On the contrary, if your account receivable cycle is 30 days and your payable is 60 days. You will always receive first before you need to pay. In the scenario of high revenue growth, the first business might not be able to survive if it is a thin margin business and have to pay the dues before receiving any revenue in return. The second business however, enjoying a negative working capital cycle, would fly in the scenario.

Arrange short-term borrow facilities. Like everything else in life, credit facilities are easier to set up when you don’t need them. Therefore, it is always a good idea to set up overdraft protection or revolving credit facilities when you do not need them. As we continue to charter through uncertain times, these fallbacks allow business owners to stay focused on what is really important — grow the business.

Have some cash buffer. The conventional wisdom is to keep 3 – 6 months of operating expenses at bay. In today’s climate though, it is better to stay on the conservative side.

Yield Optimization

The bank run earlier this year served as a powerful reminder to businesses that their deposits are not secure beyond the insurance threshold. However, the upside of this high interest rate environment is the ability to now collect 5% interest from holding Treasury bills or money market funds.

While taking advantage of the high interest rate products, it is important to consider a diversified portfolio of investments to ensure maximum safety and returns. One startup that specialize in effective treasury management is Vesto. To learn more about treasury management tools, you can also read more here.