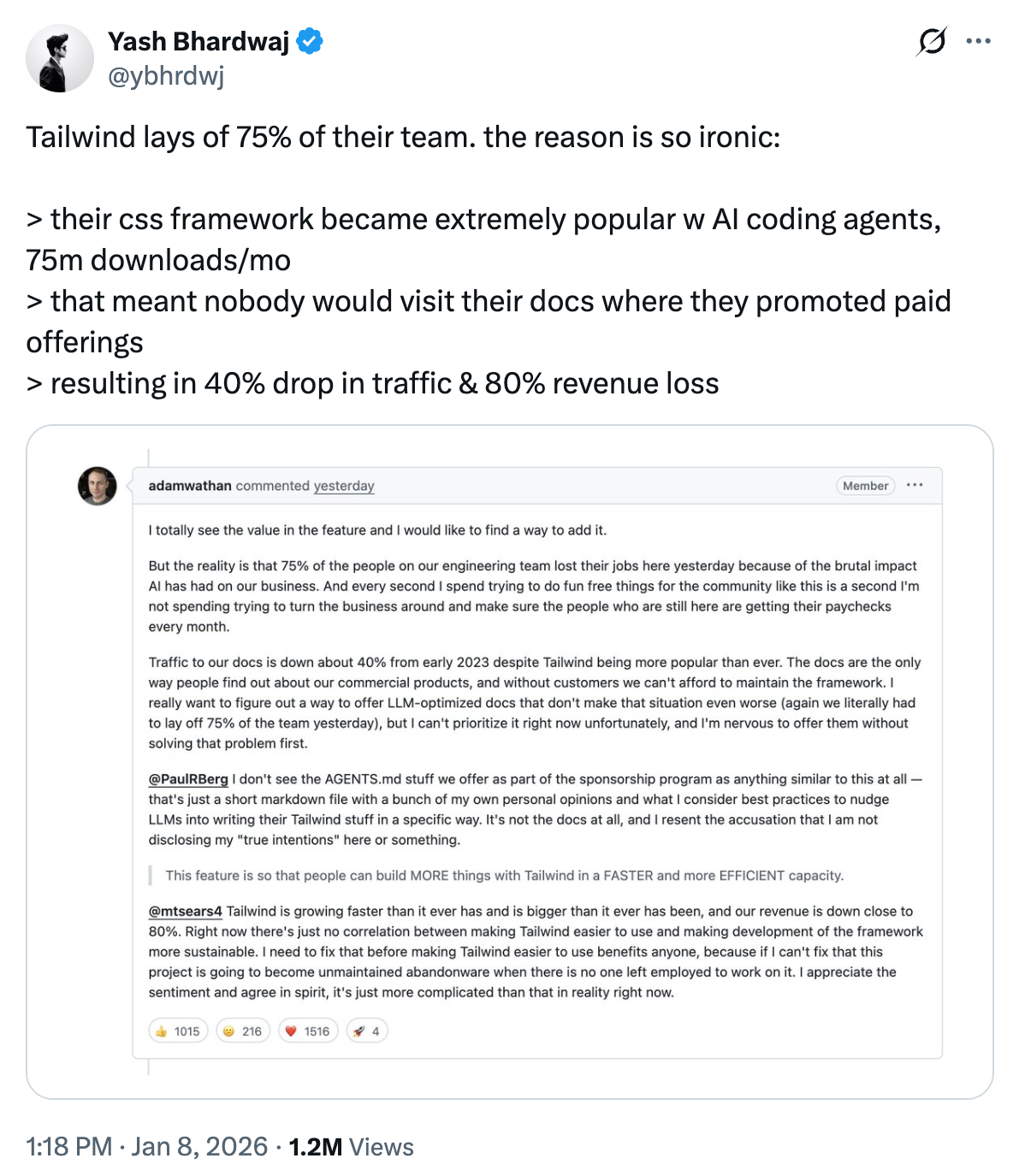

Earlier this month, Tailwind Labs, creators of one of the most widely adopted CSS frameworks in history, announced layoffs affecting 75% of its engineering team. The reason? An 80% year-over-year revenue collapse, despite record usage of Tailwind CSS. A tool that achieved near-ubiquitous product-market fit suddenly found its business model broken by AI agents.

What looks like a dev-tool tragedy is actually exposing a structural shift that fintech infrastructure players are perfectly positioned to capitalise on.

Exceptional Product-Market Fit, Fragile Monetisation

Tailwind CSS nailed product-market fit years ago. Its utility-class approach became the default for rapid, maintainable UI development at startups and enterprises alike. Usage exploded — millions of projects, massive npm downloads, and a thriving ecosystem.Tailwind Labs monetised in classic open-source style:

- Documentation sponsorships the primary revenue driver (page views → ad slots).

- Tailwind UI paid component kits for developers who wanted polished, production-ready designs faster.

This worked beautifully in a human-driven world. Developers visited the docs constantly, experimented, discovered sponsors, and often upgraded to Tailwind UI. Then AI coding agents (Copilot, Cursor, Claude, etc.) entered the picture. Suddenly, perfect Tailwind markup could be generated in seconds from natural-language prompts, without ever opening the official documentation. Docs traffic cratered. Sponsorship revenue followed. Conversions to Tailwind UI slowed as agents produced “good enough” alternatives. Usage kept climbing, but paying human engagement vanished.The result: a beloved open-source project with near-universal adoption but a business model that quietly depended on human friction.

The Extraction vs. Engagement Divide

The core issue isn’t that AI is “stealing” Tailwind, it’s that AI agents are pure extractive users.

- Engaged users (humans) browse, learn, tinker, form emotional connections, and willingly pay for convenience or prestige.

- Extractive users (agents) pull distilled knowledge at massive scale with zero engagement. They consume the cumulative wisdom embedded in class names and patterns, then disappear.

This divide breaks any monetisation strategy built on attention or human conversion funnels. Metrics like page views, sign-ups, and sessions become meaningless when your heaviest users never touch your frontend. Fintech infrastructure faces the same emerging risk. Open banking APIs, payment rails, embedded finance SDKs (many are “free” or low-cost at low volume but designed for human developers to explore, integrate, and eventually upgrade). When agentic systems start querying at scale (automated reconciliation, AI-driven underwriting, real-time pricing bots), they extract enormous value without the engagement layer that historically led to paid tiers.

The Emerging Opportunity: Make Agents Pay

The good news: agents aren’t unwilling to pay — they’re just not wired for human-style billing. The opportunity is to build monetisation that directly captures value from machine consumers. Two promising models stand out:

- Agent Tax explicit surcharges for high-volume, non-human traffic. Offer higher rate limits, deterministic outputs, or structured machine-readable feeds in exchange for premium pricing. Humans keep free/low-cost access; agents pay for the predictability and scale they need.

- Agent Wallets & Autonomous Payment Rails the more transformative path. Agents carry their own micro-wallets (via protocols like Skyfire, Paid.ai, or emerging standards) and settle tiny fees instantly per query or per outcome. A Tailwind “generation endpoint” could charge fractions of a cent for optimised, premium-enriched markup. At global scale, those micro-transactions compound into serious revenue — and turn your biggest threat (agent usage) into your primary growth driver.

This isn’t theoretical. Early infrastructure for agent payments is already live in 2026, and adoption is accelerating.For fintech, the parallel is obvious and urgent. Payment processors, data aggregators, and embedded finance platforms sit at the perfect intersection: they already handle money movement and identity. The first players to offer agent-native endpoints with built-in micro-settlement rails will capture tollbooth economics on the entire agentic economy, just as Tailwind could have if it had moved faster.Tailwind’s pain is real, but it’s also a clear signal.

The tools and protocols that monetise machine extraction at scale won’t be built by dev-tool companies alone. Fintech infrastructure has the rails, the compliance expertise, and the economic incentives to own this next layer.