In 2020, I re-engaged with Blockchain industry because of a book called “How to DeFi”. Three years later, I thought it would be interesting to do a review to see how the DeFi landscapes have changed from then to now. The book went into depth to discuss eight different use cases of DeFi, they are: stablecoins, lending and borrowing, DEX, decentralised derivatives, decentralized fund management, decentralized lottery, decentralized payments and decentralized insurance. Let’s take a look how each vertical has evolved and who are the biggest players then and now.

Stablecoins

The prices of cryptocurrencies are highly volatile. Stablecoins, as the name suggests, are cryptocurrencies pegged to other stable assets, with USD being the most popular. The peg can be maintained by owning the underlying collaterals or running an algorithm or a mix of both. The demise of TerraLuna has injected much fear into algorithm-based stablecoins. But it doesn’t mean we should abandon algorithm-based stablecoins altogether. If I am going to take a snapshot, the top 5 stablecoin as of Feb 2020 according to the book are:

| Rank | Stablecoin | Market Cap (in $mil) |

| 1 | Tether (USDT) | 4,284 |

| 2 | USD Coin (USDC) | 443 |

| 3 | Paxos Standard (PAX) | 202 |

| 4 | True USD (TUSD) | 142 |

| 5 | Dai (DAI) | 123 |

If I am going to reproduce the same table using 5th January 2023 data, it will look like this:

| Rank | Stablecoin | Market Cap (in $mil) |

| 1 | Tether (USDT) | 66,266 |

| 2 | USD Coin (USDC) | 44,237 |

| 3 | Binance USD (BUSD) | 16,616 |

| 4 | Dai (DAI) | 5,039 |

| 5 | Frax (FRAX) | 1,017 |

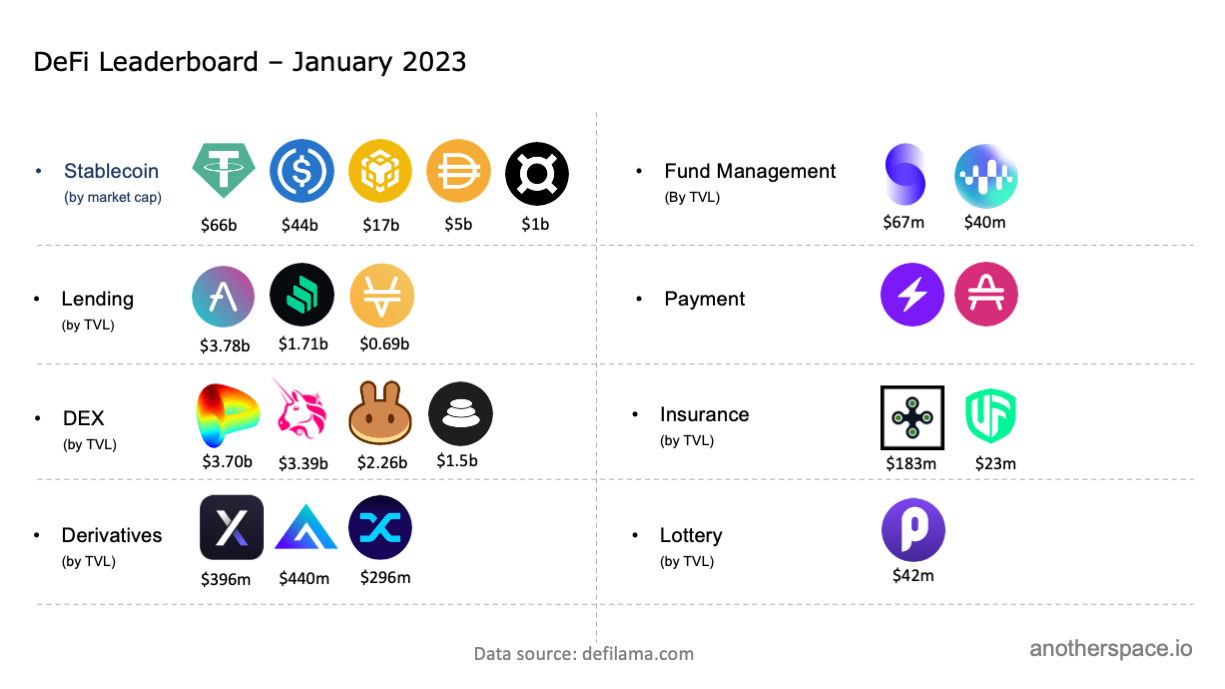

These are two very interesting tables, aren’t they? A few observations. First of all, the market has absolutely exploded. The aggregated top 5 market cap has increased from $5.2 billion in Feb 2020 to $133.2 billion as of 5th January 2022, 25.6x times of its value three years ago. Among which, USDC market cap now is 100x where it was three years ago. PAX and TUSD have dropped from Top 5 and replaced by BUSD and FRAX. Among all top 5, however, DAI remains to be the only decentralized stablecoin.

Lending and borrowing

Compound was the absolute no.1 lending protocol back in February 2020 across all chains. Fast forward to January 2023, AAVE has become the king of lending protocols with Compound remaining a significant player. At its peak, AAVE hit $19.5 billion TVL, as of today the TVL is $3.78 billion. Compound has a TVL around $1.71 bilion. Other significant lending protocols include Venus on BSC chain.

| Lending Protocol | Main Chain | TVL – 8th January | TVL- ATH |

| AAVE | Ethereum | $3.78b | $19.44b |

| Compound | Ethereum | $1.71b | $12.33b |

| Venus | BSC | $687.38m | $7.02b |

Decentralised Exchange (DEX)

It was hard to shake off the excitement when Uniswap first came around. In fact, I even fell victim to one of many Uniswap scams a couple of years ago as I was too eager to participate.

As one of the essential use cases of DeFi, the DEX landscape has changed dramatically since 2020 with many DEXs popping up on Ethereum and alternative layer one chains.

| DEX | Main Chain | TVL – 8th January | TVL – ATH |

| Curve | Ethereum | $3.70b | $24.30b |

| Uniswap | Ethereum | $3.39b | $9.77b |

| Balancer | Ethererum | $1.50b | $3.91b |

| Pancake Swap | BSC | $2.26b | $7.80b |

| Quickswap | Polygon | $161.70m | $1.42b |

| Trader Joe | Avalanche | $55.36m | $2.59b |

Decentralized Derivatives

Derivatives is a less explored vertical given its complexity. The development of a mature derivatives market more or less depends on the maturity of the spot markets, which are still very much work-in-progress. The landscape of derivatives applications didn’t change much compare to three years ago. dYdX continues to be the landmark project in decentralized derivatives. A new derivative protocol GMX on Arbitrum, however, recently overtake dYdX to become the largest by TVL. Synthetix, an exchange for synthetic assets, remains to be the leader in the lane it chose.

| Derivatives | Main Chain | TVL – 8th January | TVL – ATH |

| GMX | Arbitrum | $440.90m | $514.47m |

| dYdX | Ethereum | $396.42m | $1.12b |

| Synthetix | Ethereum | $296.25m | $2.92b |

Fund Management

Fund management yet is another less-traveled path. Set Protocol was the one discussed at length in the book. Fast forward to 2023, numbers suggest that the growth has stalled. Its peer Enzyme Finance, on the other hand, has been expanding going through this boom and bust cycle. Number-wise, Set and Enzyme seem to be head-to-head for now. I sometimes wonder the reason of the slow pick up of fund management application might be because crypto industry is built on people’s gambling money, even for institutional investors. Therefore, few will take their gambling money seriously enough to apply modern portfolio theory etc. But this will change as the real world and the crypto land continues to integrate.

Payment

As of today, payment remains to be the most prominent use case of blockchain technology. In fact, I have been so used to instant payments with close to zero fees that wire transfer has become intolerable. The 2020 book singled out Sablier Finance to exemplify blockchain’s use case in streaming payment. Three years later, although no explosive growth around streaming payment in particular, blockchain as a payment technology has been adopted by many, many more institutional players.

Decentralized Insurance

The downside risk of programmable money is code failure. In fact, the number of hacks, attacks, and exploits we heard over the past couple of years was staggering to say at least. Here enters decentralized insurance. NexusMutual was the biggest three years ago and it remains to be the biggest insurer three years later. Other insurers include Unslashed on Ethereum. As a vertical, decentralized insurance remains small and has significant upside potential.

Decentralized Lottery

As fun as it might sound, lottery is a path less chosen by project developers. Pooltogether is able to stay as leader in this space just like Nexus Mutual continue to dominate the insurance space.

The Landscape At A Glance

That’s a wrap!